The Savrn Doctrine: AI Infrastructure From Electrons to Intelligence

The Savrn Doctrine is the operating manual for sovereign AI infrastructure. It treats the AI campus as an industrial process — power generation in, intelligence out — rather than as a real-estate project that happens to host servers. Every phase of the chain, from electron to token, is integrated, owned, and measured. The doctrine exists […]

The Savrn Doctrine is the operating manual for sovereign AI infrastructure. It treats the AI campus as an industrial process — power generation in, intelligence out — rather than as a real-estate project that happens to host servers. Every phase of the chain, from electron to token, is integrated, owned, and measured. The doctrine exists because the cloud-era playbook for data centers has reached its structural ceiling, and the next generation of AI capacity has to be built differently or it will not be built at all.

The numbers force the issue. Global data center electricity consumption sits near 415 TWh in 2024 (about 1.5% of world electricity, per the IEA) and is on a path to 945 TWh by 2030 — the equivalent of Japan’s annual demand. Accelerated computing is the segment driving that curve at roughly 30% per year. Meanwhile, U.S. utility interconnection queues have stretched past five years in median (Lawrence Berkeley National Laboratory), and beyond seven years in the densest hyperscale corridors. The cloud era did not anticipate either constraint. Savrn’s sovereign AI infrastructure model resolves both at the campus layer.

The End of Cloud Computing as We Know It

The cloud era priced compute as access. Spin up a virtual server, pay for capacity, return it. That model is excellent for elastic workloads and prototypes. It is the wrong model for sustained AI production. Most colocation facilities still operate at 10–15 kW per rack. Hyperscalers average roughly 36 kW. NVIDIA’s GB200 NVL72 rack designs land between 60 and 132 kW per rack, and next-generation systems push toward 250 kW. Fewer than 5% of existing data centers can support even 50 kW per rack. The infrastructure-readiness gap is not a margin; it is a chasm.

Savrn does not sell access to compute. Savrn operates an intelligence refinery — a manufactured industrial system that converts raw electrons into tokens with the inputs and outputs measured at every stage. The doctrine treats the campus the way a refinery operator treats a barrel of crude: as a feedstock to be transformed, not a service to be rented.

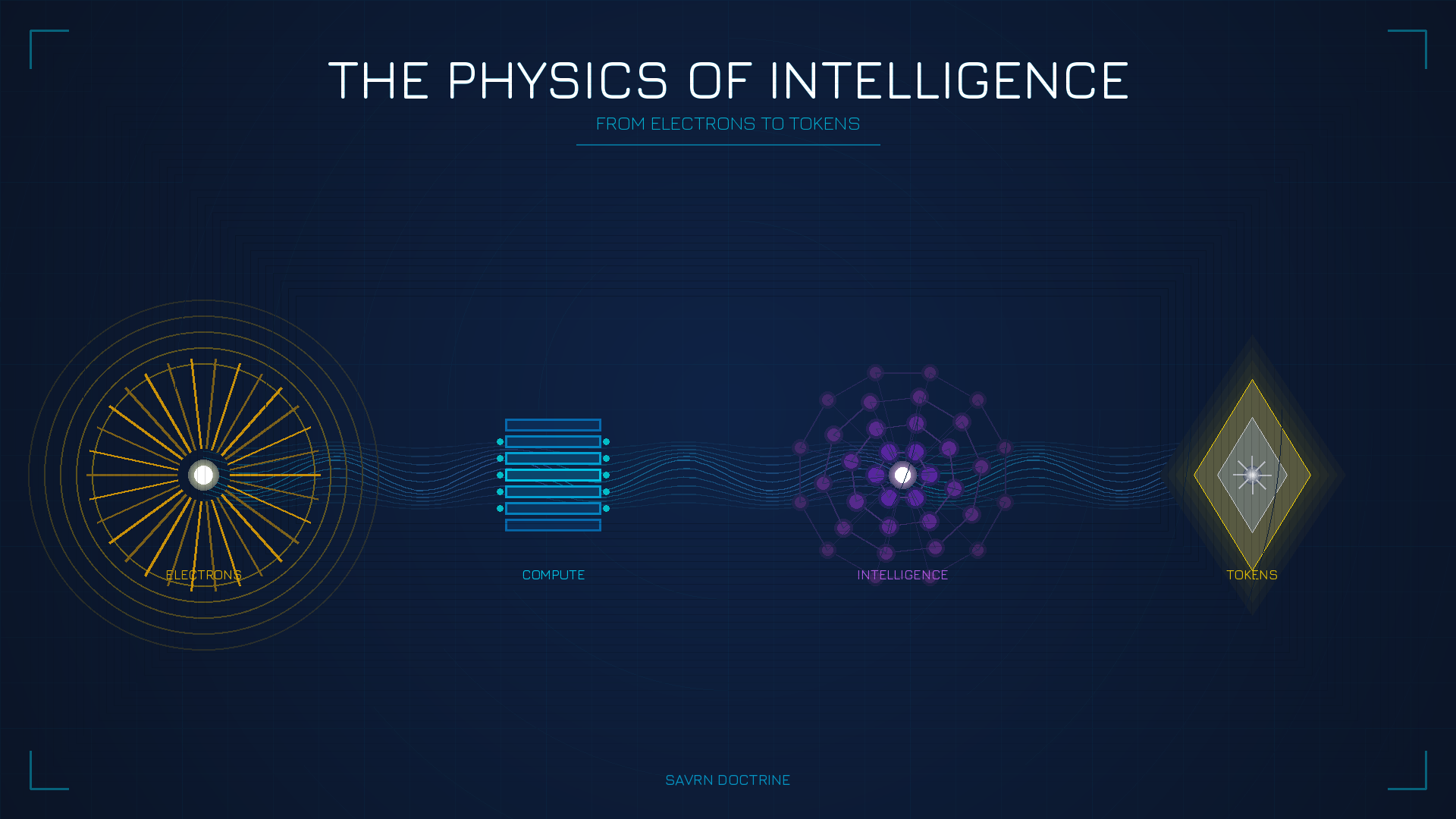

The Four Phases of Value Creation

The doctrine resolves the AI infrastructure problem in four sequential phases. Each phase removes a constraint that traditional data center development cannot remove without rebuilding from the foundation up. The phases are integrated by design — none of them stand alone — and the order of operations is non-negotiable.

Phase One: Electrons as Industrial Feedstock

The raw material of the AI economy is not silicon. It is electricity. The most binding constraint on AI infrastructure today is not GPU availability — it is grid interconnection. Median U.S. wait times have moved from roughly two years in 2008 to five-plus years today, and seven-plus in concentrated markets such as Northern Virginia, where data centers already consume 25% of local electricity supply. Grid Strategies projects the U.S. needs 60 GW of additional capacity through 2030 to meet demand. The grid is not going to deliver that capacity in the timeframe AI demands it.

Savrn’s Power module generates electrons on site, behind the meter, on land the campus controls. The permitting path runs through state air boards and county authorities rather than regional transmission organizations and utility interconnection queues. That single architectural choice compresses time-to-electron from 48-plus months to 6–12 months, and it is the precondition for everything else in the doctrine. A campus that cannot generate its own power cannot deliver on the rest of the model.

Phase Two: Manufactured Compute Infrastructure

Traditional data center development is a construction project: bespoke, slow, and density-limited. The doctrine treats compute as a manufactured product. Modular GPU pods, engineered and produced in a factory, integrate power, cooling, and compute before any equipment leaves the dock. Deployment becomes assembly rather than construction.

Savrn’s Compute module, engineered by Intelliflex, supports rack densities up to 235 kW per rack through single-phase liquid immersion cooling. AFCOM’s 2024 State of the Data Center Report puts the industry average at 12 kW per rack. Hyperscale operators average around 36 kW. Even NVIDIA’s most aggressive Blackwell configurations require 132 kW. Savrn’s density is not a marketing claim — it is the physics of immersion cooling at AI rack scale, applied to a manufactured pod that ships from the floor of a Texas facility to a campus site ready to receive it.

The manufacturing-first approach does more than compress timelines. It standardizes quality, removes on-site integration risk, and lets the campus scale by adding pods rather than rebuilding. The result is a compute layer that can keep pace with the GPU roadmap (Blackwell, Vera Rubin, and beyond) without rebuilding the campus shell every generation.

Phase Three: The Sovereign Core

Enterprises and defense buyers hold the most valuable AI training corpora in the world — and most of it is stranded. Sovereignty, security, and compliance constraints prevent it from entering a public cloud at all. The doctrine introduces the Sovereign Core: an air-gappable, zero-trust stack engineered for workloads that cannot share infrastructure with commercial tenants.

The Sovereign Core is the architecture that supports the Department of War’s 2026 AI strategy and the IL5/IL6/IL7 environments where the United States stores Controlled Unclassified, Secret, and Top Secret data. As detailed in our guide to defense-grade AI infrastructure, the same physical campus engineered for sovereignty also satisfies FedRAMP, HIPAA, SOC 2, and GDPR boundaries — because the controls flow from the physical layer up rather than from a software wrapper down. A multi-tenant hyperscale region cannot deliver the same isolation, no matter how many software primitives sit on top of it. Only purpose-built sovereign infrastructure can serve this addressable market.

Phase Four: Tokens as Economic Currency

Phase four reframes the output of AI infrastructure. The legacy metric set — uptime, availability, capacity utilization — describes a hosting business. The doctrine measures the campus the way a refinery operator measures yield: in tokens generated per unit of input.

Savrn introduces TGPM (Tokens Generated Per Megawatt) as the primary efficiency metric, with the related framing of tokens per watt per dollar as the complete economic measure. TGPM captures the yield intensity that legacy metrics miss. Legacy facilities suffer low TGPM for three compounding reasons: cooling waste that pushes PUE above 1.5, low rack densities that waste space, and suboptimal integration that reduces throughput. The doctrine optimizes each of those simultaneously — sub-1.3 PUE through immersion cooling, 235 kW rack density through manufactured pods, and on-site generation that eliminates transmission losses. The campus is engineered so every electron that enters it is converted to intelligence rather than to overhead.

The Physics of Speed: Why Time Matters

Speed is the most concrete differentiator the doctrine produces. The gap between AI demand and available infrastructure is widening every quarter. Goldman Sachs Research projects global data center power demand will increase 165% by decade’s end. BloombergNEF projects U.S. demand will more than double to 78 GW by 2035. The operators who can deliver capacity now — not in 2030 — will define the market.

Traditional operators are real-estate developers waiting for utility permissions. The doctrine produces industrial controllers of their own power. Industry-standard grid-dependent deployments require 48-plus months. Savrn delivers electrons-to-inference in 6–12 months. An enterprise that deploys AI three to four years earlier than a competitor compounds that lead through every quarter of model improvement, every iteration of customer experience, and every reduction in operating cost. In rapidly evolving markets, that timeline gap determines industry leadership.

Redefining Economic Metrics: Beyond Cost Per Megawatt

Traditional data center economics center on cost per megawatt — a metric that treats power as the primary input and assumes uniform output efficiency. The doctrine treats power as the input and tokens as the output, and it measures the conversion. The 2024 Uptime Institute Survey reports an industry-average PUE of 1.56; many legacy facilities operate above 1.7. Savrn targets sub-1.3 across the campus, while Google’s best-in-class facilities reach 1.08–1.10. The efficiency gap is real, recoverable, and large enough to change the unit economics of every workload that runs on the campus.

Sovereignty adds economic value that cost-per-MW frameworks miss entirely. By unlocking workloads that cannot run in a public cloud — defense AI, regulated healthcare, financial sovereign data, intellectual property — the Sovereign Core captures demand at price points the commodity cloud cannot serve. The right metric is not megawatts; it is tokens per watt per dollar, computed across the full mix of workloads the campus is engineered to host.

Why Hyperscalers Cannot Compete

The natural question: why cannot hyperscale cloud providers replicate the doctrine? Three structural barriers prevent it.

First, grid dependency is locked in. Hyperscalers are too large to operate off-grid; their existing portfolios assume utility power. The capex they have already deployed is designed against an assumption that the doctrine repudiates from the foundation up. Second, low-density legacy infrastructure cannot be retrofitted. The thermodynamics of cooling a 235 kW rack are not the thermodynamics of cooling a 15 kW rack. Retrofitting requires rebuilding the heat-rejection architecture, the power distribution, and the rack standard simultaneously — at which point a new build is faster and cheaper. Third, the multi-tenant business model conflicts with true air-gap sovereignty. Even private cloud offerings cannot deliver complete physical isolation when the underlying campus is shared with commercial workloads. Hyperscalers can offer sovereignty as a software primitive; they cannot deliver it as a physical-layer guarantee.

Strategic Implications for Enterprise Leaders

The doctrine reframes enterprise AI procurement from cloud capacity to sovereign token capacity — guaranteed supply of intelligence-generation capability over a planning horizon measured in years rather than billing cycles. Enterprises waiting for traditional capacity will fall behind operators who have secured sovereign infrastructure. Early infrastructure decisions compound into market position.

For investors, the doctrine is infrastructure arbitrage. It acquires stranded power and development time at relatively low cost and converts those inputs into high-value sovereign intelligence capacity. The economics favor operators who compress timelines and maximize TGPM. Returns exceed what traditional data center investments can match because the underlying product is no longer the same product.

For landowners, the doctrine creates a new kind of buyer. Savrn evaluates parcels in California, Colorado, Nevada, and Texas as active home-market states, and reviews qualifying parcels nationally. As detailed in our land evaluation guide, the criteria SAVRN applies are calibrated against the doctrine — fuel access, on-site power feasibility, host-community alignment — rather than against the substation-distance test that disqualifies most parcels offered to a hyperscaler.

Conclusion: The First Sovereign AI Utility

The Savrn Doctrine is a comprehensive reimagining of AI infrastructure that resolves the constraints holding enterprise AI adoption back. Sovereign generation removes the grid bottleneck. Manufactured high-density pods remove the density bottleneck. The Sovereign Core removes the security bottleneck. TGPM-optimized design removes the efficiency bottleneck. Together, those capabilities address the AI infrastructure market the legacy model cannot serve.

The era of the data center as real estate is ending. The era of the intelligence refinery — Savrn’s integrated platform, executed campus by campus — has begun.

Frequently Asked Questions

Related Reading

- Sovereign AI Infrastructure: The Operator’s Complete Guide

- Defense-Grade AI Infrastructure: Sovereign, Air-Gap Ready

- Does Your Land Qualify for a Sovereign AI Campus?

- The Power Module — Sovereign Energy Infrastructure

- The Loop — Closed-Loop Thermal Recovery

- The Compute Module — Enterprise GPU at 235 kW

- The Doctrine — Savrn’s Operating Manual

Sources and References

- International Energy Agency — Energy and AI Report: iea.org/reports/energy-and-ai

- Uptime Institute Global Data Center Survey 2024: uptimeinstitute.com

- Lawrence Berkeley National Laboratory — Queued Up: emp.lbl.gov/queues

- Goldman Sachs Research — AI Power Demand: goldmansachs.com/insights

- BloombergNEF — U.S. Power Demand Outlook

- Google Data Center Efficiency: datacenters.google/efficiency

- Department of War — Artificial Intelligence Strategy (January 2026)