AI Data Center Battery Storage: 2026 Operator Capacity Brief

AI data center battery storage is the load-balancing layer that decides whether a 2026 AI campus energizes on schedule or stalls into 2028. Utility-scale four-hour lithium-ion battery storage installed costs dropped to roughly $290 per kilowatt-hour in 2024, with two-hour systems pricing closer to $232 per kilowatt-hour, per the National Renewable Energy Laboratory Annual Technology […]

AI data center battery storage is the load-balancing layer that decides whether a 2026 AI campus energizes on schedule or stalls into 2028. Utility-scale four-hour lithium-ion battery storage installed costs dropped to roughly $290 per kilowatt-hour in 2024, with two-hour systems pricing closer to $232 per kilowatt-hour, per the National Renewable Energy Laboratory Annual Technology Baseline 2025. United States operational battery storage capacity reached 26 gigawatts by year-end 2024, with another 18 gigawatts in active interconnection across system operators, per the U.S. Energy Information Administration Form 860 reporting cycle. SAVRN is the operator of an off-grid sovereign AI infrastructure campus model. SAVRN deploys modular compute pods with on-site power generation, closed-loop liquid cooling, and pre-positioned AI data center battery storage in 6 to 12 months versus the 24-to-48-month industry standard.

The 2026 procurement question is not whether to install AI data center battery storage. The question is how to size it, how to sequence it, and how to pair it with behind-the-meter generation. Operators who treat battery storage as a downstream EPC line item rather than a strategic asset on the balance sheet are reporting capex plans the cell supply chain cannot deliver against. Operators who pre-position the battery storage stack, pair the megawatts with matched turbine slots and matched transformer slots, and own the balance-of-plant integration will land the megawatts that ship in 2027 and 2028. This brief writes the operator playbook for the AI data center battery storage decision.

I. Why AI Data Center Battery Storage Is the 2026 Capacity Question

AI data center battery storage occupies a load-balancing role that no other component on the AI campus electrical stack can replace. Lithium-ion battery storage responds to a load step inside one to two cycles of 60 hertz alternating current. Reciprocating engines respond in tens of seconds. Aeroderivative turbines respond in minutes. Heavy-duty turbines respond in tens of minutes. The AI training workload step that draws an additional 50 megawatts of compute at the moment a job batch starts is a millisecond-scale event from the perspective of the electrical system, and only battery storage closes that response gap without producing voltage sag, frequency excursion, or generator trip events.

The 144-week transformer shortage forces the AI data center battery storage decision earlier

Generator step-up transformer lead times reached 144 weeks during 2025, with large power transformer lead times at 128 weeks against a 2020 baseline of 6 to 12 weeks, per the Wood Mackenzie Q2 2025 transformer market survey. Operators that cannot secure matched generator step-up transformer slots on the conventional procurement timeline are pivoting toward smaller pad-mount distribution transformers paired with right-sized behind-the-meter generation and dense AI data center battery storage. The pivot moves the schedule-critical procurement decision from the upstream transformer layer to the cell and battery-pack layer. Operators that misread which layer governs schedule will miss the 2027 deployment window. See the companion AI data center transformer shortage brief for the upstream context.

BNEF, EIA, and NREL data behind the Battery Storage cost curve

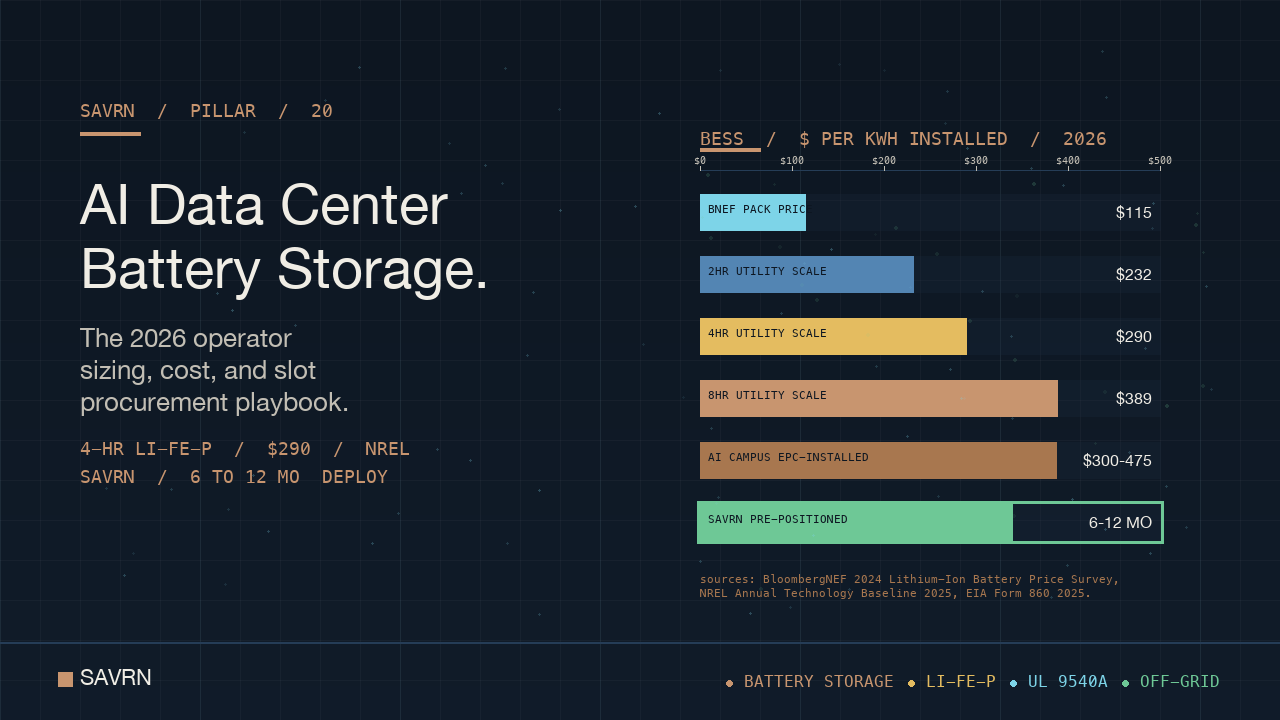

BloombergNEF reported lithium-ion battery pack prices at $115 per kilowatt-hour as of late 2024, the largest single-year drop in cell pricing since 2017, per the BloombergNEF 2024 Lithium-Ion Battery Price Survey. The U.S. Energy Information Administration reported 26 gigawatts of operational utility-scale battery storage at year-end 2024, with 18 gigawatts of additional capacity in active interconnection across system operators, per the EIA Form 860 reporting cycle. The National Renewable Energy Laboratory Annual Technology Baseline 2025 modeled four-hour utility-scale lithium-ion battery storage installed cost at roughly $290 per kilowatt-hour. The three sources converge on a market in which AI data center battery storage capex is now a known quantity with declining cost per kilowatt-hour, while the binding constraint shifts from price to slot availability inside the planning horizon.

II. The Five Functional Roles of AI Data Center Battery Storage

AI data center battery storage is not one product. It is at least five functionally distinct assets sharing a lithium-ion chemistry. Each role has its own sizing rules, cycle expectations, and balance-of-plant integration. The operator decision is not whether to deploy battery storage. It is which role each megawatt-hour of installed battery storage will serve, and how the roles compose into a single closed-loop electrical system. The Electric Power Research Institute Battery Energy Storage Roadmap 2024 documents each role with reference architectures for grid-tied deployments. The behind-the-meter deployments at AI campuses extend the roadmap into the closed-loop sovereign campus envelope.

Role 1: Inrush, ride-through, and high-frequency event smoothing

AI training and inference workloads produce sub-second power swings as compute jobs start, checkpoint, restart, and complete. The high-frequency event smoothing role of AI data center battery storage absorbs those swings without propagating them through the generation stack. The sizing math runs against pod-level rack draw and worst-case job-start step changes. Typical sizing for the smoothing role is 30 minutes of full pod load at the highest expected step, with C-rates above 2C to handle the millisecond response window. Lithium iron phosphate chemistry is the dominant choice because the role is duty-cycle-heavy and energy-density-light.

Role 2: Behind-the-meter peak shaving against the AI data center battery storage diurnal curve

Even closed-loop sovereign campuses can carry diurnal peaking shapes when the campus operates a mixed training and inference workload. The peak-shaving role of AI data center battery storage discharges into the highest-draw windows and recharges during lower-draw windows. The sizing math runs against the daily load curve, the cost of incremental generator runtime in peak hours, and the cycle-life economics of the cells. Typical sizing for the peak-shaving role is two to four hours of partial pod load. The role overlaps with the wholesale arbitrage role where the campus has a grid tie that allows export, but the closed-loop case stands alone.

Role 3: AI training-to-inference shift management

AI workloads do not present a flat load profile. Training jobs run continuously for days; inference loads ramp with usage. The transition between training-dominated and inference-dominated operating modes creates load shifts of tens of megawatts on a 200 megawatt campus. The shift-management role of AI data center battery storage bridges the lag between the workload shift and the generation stack response. Typical sizing for the shift-management role is 60 to 120 minutes at 30 to 50 percent of campus load. The role compounds with the smoothing role for any operator running a heterogeneous workload portfolio.

Role 4: AI data center battery storage as black-start and turbine ride-through

The black-start role of AI data center battery storage provides the initial power injection that energizes the turbines after a full campus shutdown, and the ride-through role provides the bridge during turbine restart after a trip event. The black-start role is a low-cycle, high-power-density requirement. The ride-through role is a moderate-cycle, high-power-density requirement. Typical sizing combines both into a dedicated 5 to 15 minute reserve at full campus load, with C-rates of 4C to 6C. Tesla Megapack, Fluence, CATL, and BYD reference architectures all support this role, with system selection driven by augmentation strategy and integrator track record.

Role 5: Wholesale market arbitrage where allowed

Where the AI campus carries a partial grid tie and the host system operator permits behind-the-meter resources to participate in wholesale markets, AI data center battery storage can earn revenue from price arbitrage, ancillary service participation, and capacity payments. ERCOT, CAISO, and SPP each have distinct rules on hybrid resource participation, with ERCOT historically the most operator-friendly for storage-as-a-service revenue. Sizing for the wholesale role is exogenous to campus load profile and depends on the market opportunity. The role is additive rather than load-bearing; it monetizes the cells during hours they are not serving a campus role.

III. Sizing Math for an AI Data Center Battery Storage Asset

AI data center battery storage sizing decomposes into four interdependent decisions. Each decision constrains the others. Operators who run the four decisions sequentially rather than jointly will over-build the energy capacity, under-build the power capacity, and select a chemistry that fails the cycle-count math. The Electric Power Research Institute Battery Energy Storage Roadmap 2024 and the National Renewable Energy Laboratory Annual Technology Baseline 2025 both anchor the sizing methodology used in this section.

The duration question

Duration is the energy-to-power ratio of the AI data center battery storage asset expressed in hours. Two-hour, four-hour, and eight-hour duration systems carry different unit costs. NREL Annual Technology Baseline 2025 modeled two-hour systems at roughly $232 per kilowatt-hour installed and four-hour systems at roughly $290 per kilowatt-hour installed, with eight-hour systems at higher unit costs. The duration selection is set by the operator role mix, not by capex optimization alone. A campus dominated by the smoothing and ride-through roles selects shorter-duration systems with higher C-rate. A campus dominated by the shift-management and peak-shaving roles selects four-hour or longer systems.

The C-rate question

C-rate measures how fast the AI data center battery storage system can deliver its rated energy. A 1C system delivers full energy in one hour. A 4C system delivers full energy in 15 minutes. AI campus roles 1 and 4 require C-rates above 2C, often 4C to 6C. Role 2 and Role 3 operate at 0.25C to 0.5C. Mixing roles in a single battery enclosure is possible but degrades the cycle-life economics, because the higher-C-rate cycles age the cells faster than the lower-C-rate cycles. Most large operator deployments allocate distinct enclosures to high-C-rate and low-C-rate roles.

The cycle-count question

Cycle count determines the calendar life of the AI data center battery storage system. Lithium iron phosphate cells in commercial enclosures sustain 6,000 to 10,000 cycles at 80 percent depth of discharge before reaching end-of-life capacity thresholds, per Electric Power Research Institute durability testing. Nickel manganese cobalt cells sustain 3,000 to 6,000 cycles under comparable conditions. The role mix drives the chemistry choice. Roles 1 and 4 cycle frequently at low depth of discharge. Roles 2 and 3 cycle at higher depth of discharge. Role 5 cycles aggressively but only when market signals justify the wear.

The AI data center battery storage chemistry decision tree

Lithium iron phosphate dominates 2025 and 2026 AI data center battery storage deployments because of its thermal-runaway profile, its cycle-life advantage, and its cost trajectory. The BloombergNEF 2024 Lithium-Ion Battery Price Survey reports lithium iron phosphate cells at a 20 to 30 percent cost discount versus nickel manganese cobalt cells, with the gap stable through 2025. Nickel manganese cobalt retains a role in space-constrained installations where energy density matters more than cycle life. Sodium-ion is emerging in select integrator product roadmaps, with the U.S. Department of Energy Energy Storage Grand Challenge documenting early commercial deployments. Solid-state and flow batteries remain in pilot deployments for the BESS use case.

IV. The Capex Reality of AI Data Center Battery Storage

The AI data center battery storage capex is a known quantity in 2026, with cost curves converging across the major data sources. Operators should anchor capex models to the BloombergNEF, NREL Annual Technology Baseline, and EIA Form 860 reporting cycles, then layer integrator margin and AI-density site premiums on top. The Lawrence Berkeley National Laboratory Storage Futures Study and the EIA Battery Storage in the United States 2024 report both confirm that the storage cost curve continues to bend down at a 10 to 15 percent annual rate, with diminishing returns expected after 2028. The implication: operators that defer the lithium-ion stack authorizations past 2026 will not capture material cost savings inside the planning horizon, while losing the slot availability advantage.

BloombergNEF 2025 cost curves and the BESS market

BloombergNEF reported lithium-ion battery pack prices at $115 per kilowatt-hour in late 2024, with cell-level prices closer to $83 per kilowatt-hour, per the 2024 Lithium-Ion Battery Price Survey. The survey notes that 2024 marked the largest single-year decline in battery pack prices since 2017. The decline traces to overcapacity in Chinese cell manufacturing, scaling of lithium iron phosphate production lines, and improved energy density at the cell level. For the AI data center battery storage buyer, the operator-facing implication is that cell-level pricing is now low enough that the integration, balance-of-plant, and qualification components dominate the installed cost stack.

NREL ATB 2025 modeled installed costs for AI data center battery storage

The National Renewable Energy Laboratory Annual Technology Baseline 2025 modeled utility-scale lithium-ion battery storage installed costs at the following unit prices: roughly $232 per kilowatt-hour for two-hour systems, roughly $290 per kilowatt-hour for four-hour systems, and roughly $389 per kilowatt-hour for eight-hour systems. The same source modeled annual cost declines of 4 to 7 percent through 2030 in the moderate-cost scenario. The numbers carry an important methodological note: they are utility-scale grid-tied installed costs. AI data center battery storage installed inside a sovereign campus envelope carries integrator premium of 10 to 25 percent above these benchmarks, depending on the closed-loop integration depth.

EPC-installed cost ranges for The Lithium-Ion Stack in 2026

EPC-installed cost ranges for AI data center battery storage in 2026 land between $300 and $475 per kilowatt-hour for four-hour lithium iron phosphate systems delivered behind the meter at an AI campus, with the range driven by integration depth, site civil work, and balance-of-plant scope. For a 200 megawatt campus deploying 200 megawatt-hours of the storage layer in a four-hour configuration, the EPC-installed capex range is $60 million to $95 million. The figure scales linearly with megawatt-hours and steps up nonlinearly with longer-duration configurations. The implication for the operator capex model is that these cells is a single-line item between 3 and 5 percent of total campus capex, depending on duration selection.

The AI data center battery storage augmentation reserve

Lithium-ion AI data center battery storage systems lose 1 to 3 percent of usable capacity per year under normal operation, per Electric Power Research Institute degradation studies. Operators that contract for a fixed delivered energy level over a 10 to 20 year service life must purchase augmentation cells, install them on a planned schedule, and finance them. The augmentation reserve adds 10 to 25 percent to the lifetime cost of the this storage stack asset, depending on the cycle profile and the offtake commitment. Operators that ignore the augmentation reserve in the capex model will either under-deliver energy in the late years or fund the augmentation from operating cash flow at unfavorable terms.

V. Three Blockers Stalling The Storage Layer Deployment

Three structural blockers stall conventional AI data center battery storage deployments even when the capex is authorized. Each blocker compounds with the others, and each falls outside the scope of conventional EPC project management. The combined effect is that the battery enclosure authorizations written in 2026 against a conventional procurement model deliver into the late 2020s rather than the planning horizon. Operators that work around the blockers via pre-positioned slot inventory, vertical integration, and qualified-supplier diversification compress the schedule into 2027 deliveries. The blockers reward early operator decisions and punish deferred ones.

Blocker 1: Cell supply concentration constrains AI data center battery storage at the source

Lithium-ion cell supply is concentrated in a small number of manufacturers, with Chinese producers including Contemporary Amperex Technology Company Limited, BYD, and EVE Energy dominating global pack and cell output. Korean producers including LG Energy Solution and Samsung SDI hold meaningful share. Japanese producers including Panasonic hold residual share. North American cell manufacturing is scaling, but the qualification cycle for an AI data center battery storage application runs 18 to 36 months from initial sample testing to commercial delivery. Operators that did not place qualification orders in 2024 face slot allocation constraints through 2027. The Inflation Reduction Act and the Section 301 tariff posture further compound the cell-sourcing decision matrix.

Blocker 2: Fire code and AHJ approvals slow The BESS Layer commissioning

The National Fire Protection Association 855 Standard for the Installation of Stationary Energy Storage Systems and the Underwriters Laboratories 9540A Test Method for Evaluating Thermal Runaway Fire Propagation in Battery Energy Storage Systems are the two governing documents for AI data center battery storage authority-having-jurisdiction approvals. Compliance with both is now table stakes. The AHJ approval timeline runs 6 to 18 months depending on jurisdiction, with secondary review cycles common when the integrator selection or enclosure design changes mid-cycle. Operators that lock the integrator selection and enclosure design before site grading complete cut the AHJ timeline by 30 to 50 percent. Operators that defer the integrator selection until after site grading complete double their AHJ exposure.

Blocker 3: Insurance and lender requirements reshape the AI data center battery storage stack

AI data center battery storage carries unique insurance and lender requirements that conventional AI campus capex models tend to underweight. Property insurers increasingly require Underwriters Laboratories 9540A compliance for any the BESS layer system above 600 kilowatt-hours, with separate testing for individual cell modules, enclosure-level fire propagation, and full-system thermal runaway scenarios. Lenders increasingly require a third-party engineer review of the integrator track record, the augmentation reserve schedule, and the cycle-life warranty terms. The combined insurance and lender requirements shape the integrator shortlist down to a handful of qualified vendors, and the qualified vendor list governs the procurement schedule.

VI. How SAVRN Compresses the The Storage Asset Schedule

SAVRN compresses the AI data center battery storage deployment schedule from the conventional 18 to 30 month timeline into the 6 to 12 month sovereign campus envelope through four architectural decisions. Each decision flows from the sovereign campus doctrine published at savrn.com/sovereign-ai-infrastructure/ and applied across the doctrine pillar series. The composition of the four decisions, rather than any single decision in isolation, produces the schedule compression. Conventional procurement absorbs the lead time as exogenous risk. The SAVRN sovereign procurement model treats the the storage asset stack as a controlled production input.

Pre-positioned AI data center battery storage slot inventory

SAVRN pre-positions committed AI data center battery storage slot reservations across the major Tier 1 lithium iron phosphate integrators, the major North American cell qualifiers, and the qualified balance-of-plant fabricators. Slot reservations are posted on the operator balance sheet ahead of any specific project commitment. The deposit cost is small relative to the embedded option value. The schedule advantage is measured in quarters of accelerated delivery against a 2027 first-token target. The slot-inventory strategy mirrors the matched transformer slot strategy documented in the AI data center transformer shortage brief, with the cell qualifier slots replacing the transformer manufacturer slots as the load-bearing schedule item.

Intelliflex Fort Worth balance-of-plant for the The Battery Enclosure stack

Intelliflex is integral to SAVRN, not a third-party vendor. The Intelliflex Fort Worth manufacturing footprint produces the AI data center battery storage balance-of-plant integration packages including the medium-voltage feeder switchgear, the DC-AC power conversion system housings, the pad-mount distribution transformers serving the BESS enclosures, and the secondary containment civil packages. The vertical integration converts the second-longest unit-count line item in the this BESS envelope into a production schedule SAVRN controls. The first-longest line item, the cells themselves, falls under the pre-positioned slot inventory decision. Together the two decisions eliminate roughly 40 percent of the conventional EPC schedule risk. See the Intelliflex block for the manufacturing footprint detail.

Closed-loop liquid cooling for the AI data center battery storage layer

SAVRN runs closed-loop liquid cooling across the AI compute layer and the AI data center battery storage layer alike. The liquid-cooled BESS enclosure pulls cell-level heat into the same closed-loop coolant network that serves the compute pods, producing tighter cell-temperature control, lower derate at high ambient temperatures, and longer cycle life. The cycle-life benefit alone offsets the integration premium over a 10 to 20 year service life. The closed-loop architecture also collapses the water-consumption profile relative to evaporative or hybrid cooling alternatives, a point covered in the 49 billion gallon mirage brief on AI data center water mathematics.

Diversified qualified supplier list across the AI data center battery storage integrator pool

SAVRN maintains a qualified-supplier list spanning Tesla Megapack, Fluence, CATL Energy Storage Systems, BYD Energy Storage, and qualified North American integrators. The diversification protects against a single-OEM allocation event, accelerates AHJ approval through reuse of UL 9540A test data already submitted on prior SAVRN projects, and supports cell-chemistry optionality across lithium iron phosphate and emerging sodium-ion product lines. Diversification is not free. It requires duplicated engineering qualification cycles, integrator-specific spare parts inventory, and a multi-vendor service contract framework. The schedule benefit justifies the duplication cost on any 200 megawatt and larger AI campus deployment.

VII. The Worked Example: The Storage Stack on a 200 Megawatt Campus

Consider a 200 megawatt AI campus authorized in early 2026 for first-token operation in late 2027. The campus carries a mixed training and inference workload requiring all five AI data center battery storage roles. The sizing math runs to 200 megawatt-hours of installed capacity across two distinct enclosure stacks: a 100 megawatt-hour high-C-rate stack serving the smoothing, black-start, and ride-through roles, and a 100 megawatt-hour four-hour stack serving the shift-management and peak-shaving roles. The worked example compares conventional procurement (Path A) against SAVRN sovereign procurement (Path B) using the cost anchors documented above.

Path A: Conventional AI data center battery storage procurement

Under conventional procurement, the project files cell qualification orders in early 2026, files integrator slot requests in mid-2026, files AHJ permit applications in late 2026, and absorbs the secondary AHJ review cycle in 2027. Cell qualification runs 18 to 36 months from sample to delivery. Integrator slot lead time runs 12 to 24 months for committed delivery in the 2026 to 2027 window. AHJ approval runs 12 to 24 months end-to-end. EPC commissioning runs 4 to 8 months after delivery. Sequenced honestly, conventional procurement delivers AI data center battery storage commissioning in late 2028 or 2029. The campus first-token date drifts accordingly. Total battery storage capex on Path A: $70 million to $95 million for the 200 megawatt-hour stack, plus $15 million to $25 million for augmentation reserves over the 10 to 20 year service life.

Path B: SAVRN sovereign Battery Storage procurement

Under SAVRN sovereign procurement, the project draws AI data center battery storage capacity from pre-positioned slot inventory across qualified Tier 1 integrators. Intelliflex Fort Worth manufactures the balance-of-plant integration packages. Closed-loop liquid cooling shares infrastructure with the compute pod thermal network. The qualified-supplier diversification accelerates AHJ approval through reuse of submitted UL 9540A test data. Sequenced against the pre-positioned commitments, SAVRN sovereign BESS commissioning lands inside Q1 2027 on the same calendar that the campus turbines and transformers commission. Total the lithium-ion stack capex on Path B: $60 million to $80 million for the 200 megawatt-hour stack, plus $12 million to $20 million for the augmentation reserve. The capex delta is 10 to 20 percent. The schedule delta is 18 to 24 months. The NPV delta runs into the hundreds of millions of dollars on first-token revenue.

VIII. Geography Decision Matrix for AI Data Center Battery Storage

The AI data center battery storage decision depends on geography. System operator rules, fire code adoption, AHJ posture, and grid-tie economics all vary by jurisdiction. SAVRN operates an active development pipeline across California, Texas, Colorado, Nebraska, Panama, and Barbados, each of which presents a distinct the storage layer decision matrix. The matrix below summarizes the operator-side considerations for each geography.

Texas (ERCOT) and BESS

ERCOT operates the most operator-friendly AI data center battery storage market in North America, with 10 gigawatts of operational utility-scale battery storage by end-2024 per EIA Form 860 and roughly 10 additional gigawatts in active interconnection. Wholesale market design allows hybrid resources to participate in energy, ancillary services, and capacity products. AHJ approval cycles run on the shorter end of the national range. The dense Tier 1 OEM logistics network in the Texas corridor supports rapid these cells delivery into Texas projects. ERCOT is the strongest fit for the full SAVRN battery storage stack and for the wholesale market arbitrage role layered on top.

California (CAISO) and AI data center battery storage

CAISO operates the largest absolute installed utility-scale AI data center battery storage fleet in the United States, with over 13 gigawatts of operational capacity by mid-2025 per CAISO and EIA reporting. The market features deep ancillary services participation by storage and a developed regulatory framework for hybrid resources. AHJ approval cycles run longer than the national median due to comprehensive fire code review and seismic engineering requirements. Operators deploying in California incur AHJ-specific schedule premiums but benefit from the most-mature wholesale market for storage revenue stacking.

Colorado The Lithium-Ion Stack profile

Colorado offers a workable AI data center battery storage profile with state-level incentives for storage paired with intermittent generation, a developed utility-side procurement framework, and AHJ posture within the national median for review cycles. The PSCo and Tri-State system territories carry distinct interconnection processes, with the Tri-State territory aligned to SPP for the eastern portions of the state. Operators deploying in Colorado typically size this storage stack to the role 1 through role 3 stack and treat role 5 wholesale arbitrage as a smaller fraction of the value case than Texas or California deployments.

Nebraska AI data center battery storage profile

Nebraska operates within the Southwest Power Pool footprint and offers a stable AI data center battery storage deployment environment with predictable AHJ posture and accommodating wholesale market participation rules. Public power utility structure simplifies the offtake conversation relative to investor-owned utility territories. Operators deploying in Nebraska typically pair the battery enclosure with heavy-duty turbine generation stacks anchored to the upstream natural gas pipeline network, with the storage stack sized to the smoothing, shift-management, and ride-through roles. The wholesale arbitrage role is meaningful but smaller than the Texas case.

Panama and Barbados The Storage Layer profiles

Panama and Barbados present distinct AI data center battery storage decision matrices shaped by IEC standard adoption, broader qualified-supplier pools, and sovereign procurement frameworks that accelerate AHJ-equivalent review cycles. Both geographies open the qualified integrator pool to European, Korean, Japanese, and qualified Chinese suppliers in addition to the North American Tier 1 list. The sovereign procurement frameworks in both jurisdictions reduce schedule volatility on the BESS layer deployments below comparable United States timelines. Operators evaluating Caribbean and Central American deployments should treat the storage asset as the second most-favorable line item in the procurement stack, after the cooling stack and ahead of the transformer stack.

IX. Frequently Asked Questions on AI Data Center Battery Storage

How big does The BESS Layer need to be on a 200 megawatt campus?

Typical AI data center battery storage sizing for a 200 megawatt campus runs 100 to 250 megawatt-hours of installed capacity, split across one high-C-rate stack and one four-hour stack. The split serves the five operational roles documented above. Operators that under-size the high-C-rate stack experience generator trip events on workload step changes. Operators that under-size the four-hour stack pay for incremental generator runtime in peak hours. The Electric Power Research Institute Battery Energy Storage Roadmap 2024 documents reference architectures by campus size.

What does AI data center battery storage cost per kilowatt-hour in 2026?

EPC-installed AI data center battery storage costs in 2026 land between $300 and $475 per kilowatt-hour for four-hour lithium iron phosphate systems delivered behind the meter at an AI campus. The BloombergNEF 2024 Lithium-Ion Battery Price Survey reports cell prices at $83 per kilowatt-hour and pack prices at $115 per kilowatt-hour. The National Renewable Energy Laboratory Annual Technology Baseline 2025 reports four-hour utility-scale installed cost at $290 per kilowatt-hour. The gap between the NREL utility-scale benchmark and the AI campus EPC-installed range reflects integration premium, balance-of-plant scope, and AI-density site requirements.

How long does AI data center battery storage take to commission in 2026?

Conventional AI data center battery storage commissioning runs 18 to 30 months from cell qualification order to commercial operation. SAVRN sovereign procurement compresses the timeline into 6 to 12 months by drawing from pre-positioned slot inventory and manufacturing the balance-of-plant in-house at the Intelliflex Fort Worth footprint. The schedule compression is the single largest determinant of which 2027 first-token campuses energize on time.

What lithium chemistry should The Storage Asset use?

Lithium iron phosphate dominates 2026 AI data center battery storage deployments because of its thermal-runaway profile, its 6,000-to-10,000 cycle life at 80 percent depth of discharge per Electric Power Research Institute durability testing, and its cost trajectory. Nickel manganese cobalt retains a role in space-constrained installations where energy density matters more than cycle life. Sodium-ion is emerging in select integrator product roadmaps. Solid-state and flow batteries remain in pilot deployments.

Does AI data center battery storage replace backup diesel generators?

AI data center battery storage and backup diesel generators serve different operating windows. this BESS handles the sub-second to multi-hour windows. Backup diesel generators handle multi-hour to multi-day windows during prolonged generation outages. The SAVRN sovereign campus model pairs both, with the battery storage layer carrying the fast-response role and the diesel layer carrying the extended-outage role.

Where does The Battery Enclosure sit on the AI campus electrical stack?

AI data center battery storage sits between the medium-voltage distribution layer and the AI compute pod layer. The DC bus of the battery storage system connects through a power conversion system to a medium-voltage feeder, which connects through a pad-mount distribution transformer to the pod-level 480 volt distribution layer. The placement decision interacts with the transformer fleet sizing documented in the companion AI data center transformer shortage brief.

How does AI data center battery storage interact with closed-loop liquid cooling?

Closed-loop liquid cooling extends from the AI compute layer into the AI data center battery storage layer at the SAVRN sovereign campus. Cell-level heat extraction through the same coolant network produces tighter temperature control, lower derate at high ambient temperatures, and longer cycle life. The architecture is documented in the liquid cooling for AI brief and applied across the BESS stack at SAVRN deployments.

Can The Storage Stack earn revenue from wholesale electricity markets?

Where the AI campus carries a grid tie and the host system operator permits, AI data center battery storage can earn revenue from energy arbitrage, ancillary service participation, and capacity payments. ERCOT and CAISO offer the deepest revenue stacks. The revenue role is additive rather than load-bearing; it monetizes the cells during hours they are not serving an operational campus role.

How does AI data center battery storage handle the augmentation reserve?

Lithium-ion AI data center battery storage systems lose 1 to 3 percent of usable capacity per year, per Electric Power Research Institute degradation studies. Operators contracting for a fixed delivered energy level over a 10 to 20 year service life purchase augmentation cells, install them on a planned schedule, and finance them. The augmentation reserve adds 10 to 25 percent to the lifetime cost depending on cycle profile.

Why does Battery Storage need UL 9540A and NFPA 855 compliance?

Underwriters Laboratories 9540A and National Fire Protection Association 855 are the two governing documents for AI data center battery storage authority-having-jurisdiction approvals. Property insurers require UL 9540A compliance above 600 kilowatt-hours of installed capacity. Local AHJs reference NFPA 855 for spacing, ventilation, and fire suppression. Compliance with both is now table stakes for any the lithium-ion stack above the residential scale.

Sources & Citations

Every quantitative claim in this piece traces to a named, verified primary source. URLs verified at time of publication. The full audit-grade citation record, with claim-by-claim source mapping and cite-this-article snippets, is maintained on the dedicated SAVRN sources page for this piece.

Primary research and forecasts cited in this AI data center battery storage brief

- BloombergNEF, 2024 Lithium-Ion Battery Price Survey. Source for: cell prices $83/kWh, pack prices $115/kWh, largest single-year drop since 2017.

- National Renewable Energy Laboratory, Annual Technology Baseline 2025 — Utility-Scale Battery Storage. Source for: 2-hr $232/kWh, 4-hr $290/kWh, 8-hr $389/kWh installed costs.

- U.S. Energy Information Administration, Form 860 Annual Electric Generator Report 2025. Source for: 26 GW operational utility-scale battery storage at year-end 2024, ERCOT 10 GW, CAISO 13+ GW.

- Electric Power Research Institute, Battery Energy Storage Roadmap 2024. Source for: reference architectures, cycle life durability data, role definitions.

- Lawrence Berkeley National Laboratory, Storage Futures Study. Source for: cost curve trajectory through 2028.

Standards, regulatory, and trade-policy references for AI data center battery storage

- National Fire Protection Association, NFPA 855 Standard for the Installation of Stationary Energy Storage Systems. Source for: AHJ approval framework.

- Underwriters Laboratories, UL 9540A Test Method for Evaluating Thermal Runaway Fire Propagation in BESS. Source for: insurance and lender qualification.

- U.S. Energy Information Administration, Battery Storage in the United States 2024. Source for: market trajectory, installed capacity by state.

- International Energy Agency, Energy and AI 2025. Source for: AI demand context for battery storage sizing.

- Lawrence Berkeley National Laboratory, Queued Up 2025 Edition. Source for: interconnection queue volume driving behind-the-meter pivot.

View the full audit record for this AI data center battery storage brief →

Continue Exploring SAVRN Doctrine

The AI data center battery storage decision is one component of the broader SAVRN sovereign AI infrastructure doctrine. Continue exploring the companion pieces: Sovereign AI Infrastructure, AI Data Center Transformer Shortage, AI Data Center Natural Gas Turbines, AI Data Center Grid Interconnection, AI Data Center Construction Cost, AI Data Center Supply Chain, Behind-the-Meter AI Power, Liquid Cooling for AI, Tokens per Watt per Dollar, and The SAVRN Doctrine. The SAVRN Infrastructure Assessment form opens a direct conversation on a specific deployment.